When AI Reproduces Culture — and Consumes the Planet

Artificial intelligence is no longer simply augmenting creativity — it is replicating it.

Over the past two years, generative AI systems have reached a point where they can convincingly reproduce the aesthetic codes of past television formats, musical genres, and visual cultures. Vintage broadcast styles from North American network television, European public-service programming formats, Latin American telenovela pacing, Japanese anime visual grammar, early-2000s global pop production textures, even specific narrative pacing patterns once characteristic of traditional media — all can now be generated synthetically at industrial scale.

The implications are not only cultural. They are structural, economic, and environmental.

We are entering an era where AI-generated content is no longer marginal. It is becoming dominant. The scale is unprecedented.

The Industrialization of Synthetic Culture

In music streaming alone, the acceleration is measurable. According to Deezer’s official investor communications (Q3 2025 results), nearly 30% of the tracks uploaded daily to the platform in September 2025 were fully AI-generated.

By early 2026, Deezer reported that approximately 60,000 AI-generated tracks were being uploaded every day, representing close to 40% of daily uploads (Deezer Press Release, January 2026, published via Euronext).

Within the streaming platforms with the most subscribers worldwide — Spotify, Apple Music, Amazon Music, etc. — there is no universal position yet, and some major labels are simultaneously exploring collaborations with AI music startups while defending copyright in court.

The phenomenon is not limited to music. Industry observers and analysts have suggested that a substantial portion of newly uploaded short-form and long-form videos on major platforms are now fully synthetic. While precise audited numbers for YouTube remain difficult to verify publicly, the trajectory across platforms indicates the same pattern: generative systems are scaling faster than traditional creative pipelines.

According to the British newspaper The Guardian, December 2025, a large independent study by the video-editing platform “Kapwing” found that a “significant portion” of the content recommended to new YouTube users is effectively “AI slop” — meaning algorithmically generated, low-effort, synthetic videos: More than 20 % of the videos shown to new YouTube users are “AI slop” — low-quality AI-generated content targeted to maximize views rather than provide real value. Among the top 15,000 global channels surveyed, “278 channels consisting entirely of such content” collectively claimed 63 billion views and 221 million subscribers, generating an estimated $117 million in revenue.

This analysis suggested that between 21 % and 33 % of videos recommended across YouTube’s feeds in late 2025 might consist of “AI slop” or similar mass-produced automated content.

More strikingly, an Ipsos survey conducted in partnership with Deezer found that 97% of listeners were unable to distinguish AI-generated music from human-created tracks.

This is the turning point.

AI is no longer “obviously artificial.” It has absorbed stylistic memory — the cultural DNA of prior decades — and can now reproduce it convincingly.

The Hidden Cost: Energy

Generative AI does not operate in abstraction. It runs on data centers — vast physical infrastructures consuming enormous amounts of electricity. The same systems generating synthetic culture at scale are driving a surge in energy demand — often met by carbon-intensive sources.

According to the International Energy Agency (IEA), data centers are becoming a significant and rapidly growing component of global electricity demand. The IEA has highlighted that a large AI-focused data center can consume electricity equivalent to the annual consumption of about 100,000 households.

In 2024, global data center electricity consumption was about 415 terawatt-hours (TWh), which amounted to around 1.5 % of global electricity use. The IEA notes that this figure has grown by roughly 12 % per year in recent years and is expected to more than double to about 945 TWh by 2030 under its base scenario, largely due to AI and digital services growth.

The IEA also points out that AI workloads — typically run on high-performance accelerated servers — are a key driver of this growth, with accelerated servers projected to grow electricity demand by about 30 % annually in the base case scenario.

An academic paper titled “The Environmental Impact of AI Servers and Sustainable Solutions” reinforces the projected trajectory of data center growth and electricity demand. The study indicates that global electricity consumption from data centers could roughly double by 2030 as AI workloads expand. Published on arXiv in 2026, the research highlights that electricity use linked to AI and data center operations may increase even further depending on deployment intensity and hardware efficiency improvements.

While data center infrastructure is increasingly connected to renewable sources, fossil fuels continue to provide a substantial portion of the electricity powering them: according to IEA-based analysis, nearly 60 % of the electricity consumed by data centers globally comes from fossil fuels, primarily coal and natural gas, with renewables (27 %) and nuclear (15 %) making up the remainder.

This aligns with the broader IEA assessment that while renewable deployment is expanding rapidly, existing fossil generation remains dominant in data center power mixes, especially in key regions such as China and the U.S., making the environmental impact of data center expansion a near-term concern.

This is the structural contradiction.

The main concern with artificial intelligence is not a science-fiction scenario where it turns against humans, but rather the impact it can have on our environment and its potential contribution to climate change.

The environmental implications of generative AI are not abstract — they are systemic and infrastructure-level:

1. Increased electricity load. AI workloads run continuously on high-power servers, and as adoption scales across media, finance, healthcare, and entertainment, data centers are becoming one of the fastest-growing sources of electricity demand globally.

2. Greater short-term reliance on gas turbines. To meet peak loads from hyperscale AI facilities, many grids — especially in the U.S. and parts of Asia — depend on natural gas, even when renewable supply is available.

3. Pressure to expand nuclear and fossil capacity. Continuous, power-intensive AI workloads are driving governments to consider new nuclear or thermal plants to ensure reliable baseload, linking energy policy with digital infrastructure strategy.

4. Rising embedded carbon in infrastructure. Beyond operations, building and maintaining servers, cooling systems, and transmission networks generates substantial lifecycle emissions, often undercounted in energy discussions.

Taken together, these dynamics mean that generative AI is not simply a software phenomenon. It reshapes physical infrastructure investment, grid planning, fuel mix decisions, and industrial supply chains. In energy terms, culture is no longer weightless.

Generative culture, it turns out, is materially physical.

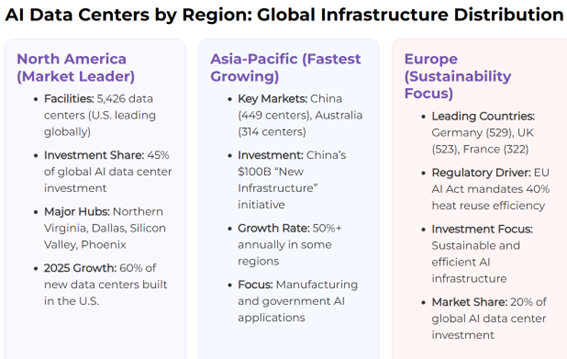

AI Data Center Statistics

AI data center statistics are redefining the future of technology, fueling everything from ChatGPT to groundbreaking AI innovations. These centers are no longer just supporting cloud computing, they’re set to power the entire AI-driven economy by 2026.

In 2024, AI data center investments soared to an eye-popping $57 billion, with projections surging beyond $200 billion annually by 2030. This market is growing at an extraordinary 28.3% rate, outpacing the 11.24% growth of traditional data centers by a wide margin.

This report dives into the AI data center statistics shaping the next phase of global infrastructure. From mind-blowing energy consumption to unprecedented water usage, the scale of these AI hubs is as awe-inspiring as it is alarming.

Curious about the most jaw-dropping stat? By 2030, AI training workloads are projected to consume up to 70% of global data center capacity.

In just a few short years, the landscape of AI data centers has rapidly expanded. By March 2026, there are around 11,800 data centers worldwide, with an increasing number incorporating AI-specific infrastructure. Unlike traditional data centers that typically handle 10-15 kW per rack, AI data centers need between 40-250 kW per rack to support the heavy computational demands of machine learning models.

The investment landscape for AI data centers has reached unprecedented levels. In 2024, AI-specific investments totaled $57 billion, and projections suggest this will balloon to a staggering $5.2 trillion by 2030.

The biggest tech players are leading the charge:

- Microsoft: Committing $80 billion in fiscal 2025 for AI-enabled data centers.

- Amazon: Planning over $100 billion in AI infrastructure expansion.

- Google: Pledging $75 billion globally for data center infrastructure.

- Meta: Increasing capital expenditure to $65-72 billion for AI facilities.

The most ambitious project? The Stargate initiative, a $500 billion joint venture involving OpenAI, Oracle, SoftBank, and others, is aiming to deploy a 5 GW data center by 2028.

AI data centers are redefining global technology infrastructure, combining unprecedented investment, energy demand, and computational scale to power the next era of innovation.

INCONCRETO’s Strategic Vision

At INCONCRETO, we view this not as a moral panic — but as a structural transition.

AI is now capable of replicating cultural codes at industrial scale. That changes creative markets. But it also changes energy markets.

The convergence of:

- Synthetic media production

- Platform economics

- Data center infrastructure expansion

- Fossil-linked electricity generation

creates a systemic issue, not a sectoral one.

The question is not whether AI will continue to expand. It will.

The question is whether governance, infrastructure strategy, and sustainability frameworks will evolve at comparable speed.

If not, the cost of infinite digital creativity may be measured in megawatts — and in carbon.

And that is not a cultural debate.

It is an industrial one.

For further reading, you may consult these sources:

- AP News – Suno, Udio AI Music and Record Labels Debate

https://apnews.com/article/suno-udio-ai-music-record-labels-849a2d59eab89072154ab32b4db06284 - Euronext – Deezer Investor Relations (Q3 2025 Results)

https://live.euronext.com/en/product/equities/fr001400ayg6-xpar - The Guardian – Study: AI-Generated Videos on YouTube

https://www.theguardian.com/technology/2025/dec/27/more-than-20-of-videos-shown-to-new-youtube-users-are-ai-slop-study-finds - Deezer Newsroom – Deezer-Ipsos Survey on AI Music

https://newsroom-deezer.com/2025/11/deezer-ipsos-survey-ai-music/ - International Energy Agency (IEA) – Energy and AI Report

https://www.iea.org/reports/energy-and-ai/energy-demand-from-ai - Eco-Business – AI, Data Centers and Energy Use

https://www.eco-business.com/news/ai-five-charts-that-put-data-centre-energy-use-and-emissions-into-context/ - arXiv – The Environmental Impact of AI Servers and Sustainable Solutions (Preprint)

https://arxiv.org/abs/2601.06063 - Ttms.com – Growing Energy Demand of AI Data Centers (2024–2026)

https://ttms.com/growing-energy-demand-of-ai-data-centers-2024-2026/ - AllAboutAI – AI Data Center Statistics and Trends

- https://www.allaboutai.com/resources/ai-statistics/ai-data-centers/

Latest News

© INCONCRETO. All rights reserved. Powered by AYM