Construction Robotics and the Transformation of Industrial CAPEX

Construction’s Productivity Model is Under Pressure

Global construction demand continues to expand, but the industry’s operational model is struggling to scale at the same pace.

According to McKinsey, driven by infrastructure modernization, energy transition programmes, urban development, and industrial reshoring strategies, global construction spending is expected to rise from $13 trillion in 2023 to $22 trillion by 2040.

This growth trajectory places construction at the centre of the transition toward lower-carbon economies. Renewable energy projects, transportation infrastructure, industrial facilities, housing, and grid modernization all depend on the sector’s ability to execute complex projects at scale.

However, the industry is facing structural constraints that directly affect its delivery capacity. Labour shortages are intensifying globally across construction and skilled trades. In the United States alone, the sector is projected to require nearly 350,000 additional workers in 2026, while the UK construction industry is expected to need close to 48,000 new workers annually through 2029. Australia is also facing severe shortages, with industry estimates pointing to a gap of more than 116,000 construction workers to meet national housing targets. The European Builders Confederation (EBC) recently stressed to what extent across the EU labour and skills shortages are increasingly affecting construction, infrastructure, energy-efficiency renovation and digital transition projects, driven by ageing workforces, insufficient vocational training and rising investment demand.

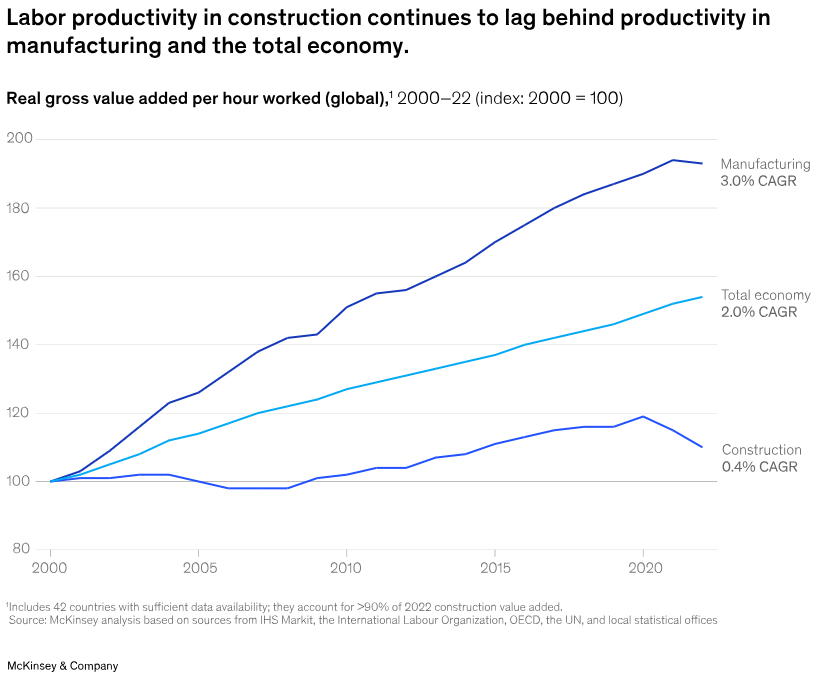

These tensions are amplified by a long-standing productivity challenge. Despite rising demand and accelerated investment needs, construction productivity growth has significantly lagged behind manufacturing for decades, while projects themselves have become more technically demanding, more regulated, and more dependent on coordination.

McKinsey analysis highlights the scale of this gap. Between 2000 and 2022, productivity in construction improved only marginally at the global level, while manufacturing achieved substantially stronger gains over the same period.

This imbalance creates growing pressure on the industry’s delivery model. Construction companies are expected to execute larger and more sophisticated projects under tighter timelines, while operating with constrained labour availability and limited productivity gains.

As a result, the industry is confronted with a structural question: how can construction scale capacity without proportionally scaling labour intensity, delays, and operational risk?

Robotics is emerging as part of a broader industrial response aimed at improving execution consistency, continuity, and project control.

When Execution Becomes the Strategic Challenge

Thus, construction sites remain highly fragmented environments where productivity depends on the alignment of multiple trades, equipment fleets, subcontractors, and changing site conditions.

Unlike manufacturing facilities, field operations must continuously adapt to unstable physical contexts, weather conditions, logistical constraints, and evolving project requirements. This dependence on manual coordination contributes directly to delays, rework, safety exposure, and variability.

Recent analysis from Texas A&M University highlights how robotics is gradually being deployed to address these practical constraints directly, particularly in repetitive, hazardous, and precision-dependent activities across construction field operations.

Within this context, autonomous and semi-autonomous technologies are reshaping how construction activities are executed on site.

Earthmoving and excavation provide a clear illustration. These activities are repetitive, labour-intensive, highly exposed to safety risks, and critically dependent on precision and execution consistency. They also directly affect project schedules and downstream coordination across the construction site.

Companies such as the American Built Robotics are addressing these constraints by retrofitting conventional heavy machinery with autonomous guidance and control capabilities. Excavators equipped with robotics, GPS positioning systems, sensors, and AI-based software can perform trenching and excavation tasks with limited human intervention while maintaining highly precise operational parameters. Therefore, existing machinery fleets are transformed into intelligent assets capable of executing repetitive tasks continuously and with greater consistency.

Such concrete deployments are already demonstrating measurable impacts. Built Robotics has implemented autonomous excavation systems across solar infrastructure and utility projects, improving trenching productivity while reducing operator exposure to hazardous situations.

Construction layout operations are equally affected. Companies such as California-based Dusty Robotics are deploying autonomous field-printing robots capable of translating digital building models and technical design plans directly onto construction floors with high precision. By automating layout processes traditionally performed manually, these systems improve trades, reduce rework, and strengthen alignment between digital project planning and on-site deployment.

The same trajectory is becoming visible across broader construction operations, because autonomous monitoring systems, robotic layout technologies, drone-assisted surveying, and AI-enabled machinery coordination are steadily redefining project delivery on construction sites.

A deeper operational evolution is concretely taking place, with robotics introducing greater continuity, precision, and organisation into an industry historically characterized by fragmentation and variability.

The Construction Site Becomes an Interconnected Environment

Traditional construction sites are organized around sequences of independent activities performed by multiple specialized actors. Robotics introduces a different logic, where execution relies on coordination between machines, software, sensors, and real-time data flows.

Field operations are evolving toward environments where:

- robotic equipment operates simultaneously across multiple activities

- machinery performance is monitored continuously through software layers

- positioning, management, and quality controls are synchronized through digital systems

- site-level adjustments can be made in real time

This evolution changes how construction activity itself is managed, becoming measurable, traceable, and coordinated across the project lifecycle.

A growing number of systems focus on precision tasks that directly connect digital project models with physical execution on site. In BIM-linked robotic construction systems, machines are capable of executing operations such as layout marking, drilling, and fastening based directly on digital building models. These systems interpret design data and translate it into precise on-site actions, reducing the need for manual interpretation of technical drawings.

A notable example is the Collaborative On-Site Construction Robot developed through industry collaborations such as Skanska and HAL Robotics, which integrates BIM data with autonomous navigation and robotic drilling capabilities to execute anchoring and installation tasks on site.

This kind of integration shifts construction from sequential tasks toward a continuously coordinated functional process, where field activities are informed by real-time data and digital planning inputs.

As a result, construction sites function more as interconnected frameworks, where machinery, software, and field operations jointly contribute to execution performance.

This shift improves visibility and enables earlier detection of deviations, more consistent coordination between project phases, and improved control under changing site conditions.

As robotics adoption expands, the strategic value of construction operations depends on the ability to orchestrate these interconnected layers.

CAPEX Reimagined: When Robotics Redesigns Construction Investment Logic

As construction operations evolve toward robotics-enabled deployment models, capital expenditure logic is also being redefined.

Historically, construction CAPEX focused on machinery acquisition, fleet expansion, utilization rates, and depreciation cycles. Competitive advantage was largely driven by equipment volume and labour deployment capacity.

Robotics gradually shifts investment priorities toward the quality of development that assets make possible, rather than the assets themselves. Capital allocation increasingly reflects requirements for precision, operational continuity, and management across complex and variable projects.

This evolution is evident in emerging industry trajectories. Robotics and embodied AI are considered as long-term enablers of structured and repetitive tasks, although large-scale deployment remains at an early stage of development.

At the same time, retrofit approaches such as those developed by Built Robotics illustrate a shift toward upgrading existing equipment through autonomous capabilities, sensors, and software layers rather than replacing entire fleets.

CAPEX is now structured around four interdependent dimensions:

- Investment emphasis moves from asset ownership to execution capability, defined by precision, autonomy, and coordination potential.

- Equipment lifecycles extend through digital upgrades, connectivity, and predictive maintenance functions.

- Productivity becomes driven by execution consistency and automation rather than labour scaling.

- Asset value is assessed through interoperability within connected digital and physical environments.

Together, these shifts point to a redefinition of CAPEX: from financing physical capacity toward investing in coordinated, software-enabled environments designed to operate under increasing project complexity.

Implications for Strategic CAPEX Decisions

In construction, robotics is progressively redesigning the structure and purpose of industrial investment.

Capital allocation illustrates the need to support adaptable and coordinated execution across complex and evolving project contexts. In this context, competitive positioning is determined by the ability to orchestrate integrated capabilities across equipment, software, and field implementation.

For decision-makers, this shifts investment evaluation toward system-level performance rather than isolated asset metrics. While traditional indicators such as fleet size and utilization remain relevant, they are interpreted through specific outcomes linked to delivery reliability and control.

Robotics reinforces a broader industrial trend: the move toward construction models where performance depends on the ability to manage variability, coordinate interdependent activities, and sustain operational coherence across the project lifecycle.

INCONCRETO’s Value Proposal: Shaping the Future of Construction Execution

The rise of robotics in construction reflects a broader transformation of how projects are planned, coordinated, and executed across increasingly complex environments.

INCONCRETO supports organizations in addressing this evolution by connecting technological innovation with impactful performance and long-term investment strategy. This includes helping clients assess where robotics and intelligent technologies can improve project delivery, strengthen coordination across field operations, and enhance the resilience of construction activities under changing site conditions.

By combining expertise in industrial operations, digital integration, and organizational transformation, INCONCRETO helps construction stakeholders structure models where equipment, software, data flows, and processes function coherently throughout the project lifecycle. Through this approach, companies can improve execution reliability and align capital investment decisions with long-term performance objectives across gradually more sophisticated construction programmes.

For further reading, you may consult these sources:

- Delivering on construction productivity is no longer optional, by McKinsey & Co.

- Embracing Construction Robotics: The Future of Construction Field Operations, by Texas A&M University

- How Built Robotics Made Excavators Autonomous on Active Job Sites, by Robotomated

- Autonomous Excavation: GPS-Guided Earthmoving Without Operators, by Romotomated

- BIM-to-Field Robots: How Dusty Robotics and Hilti Are Digitizing Job Sites, by Robotomated

- BIM-driven robotics in construction: A systematic review of integration methods, applications, and future directions, in The Journal of Intelligent Construction

- Skanska unveils BIM-linked construction site robot, by Construction Management

- Humanoid robots in the construction industry: A future vision, by McKinsey & Co.

Latest News

© INCONCRETO. All rights reserved. Powered by AYM